It’s the third-to-last race at a midweek meeting. You’re £180 down on the day. The card has two more runners with the form to win, and somewhere in the back of your head a calculator has already started running the stake that gets you back to level. The next bet won’t be the bet you’d planned at breakfast.

It’s the third-to-last race at a midweek meeting. You’re £180 down on the day. The card has two more runners with the form to win, and somewhere in the back of your head a calculator has already started running the stake that gets you back to level. The next bet won’t be the bet you’d planned at breakfast.

Every serious punter recognises this moment. Most have lost more bankrolls to it than to bad form study.

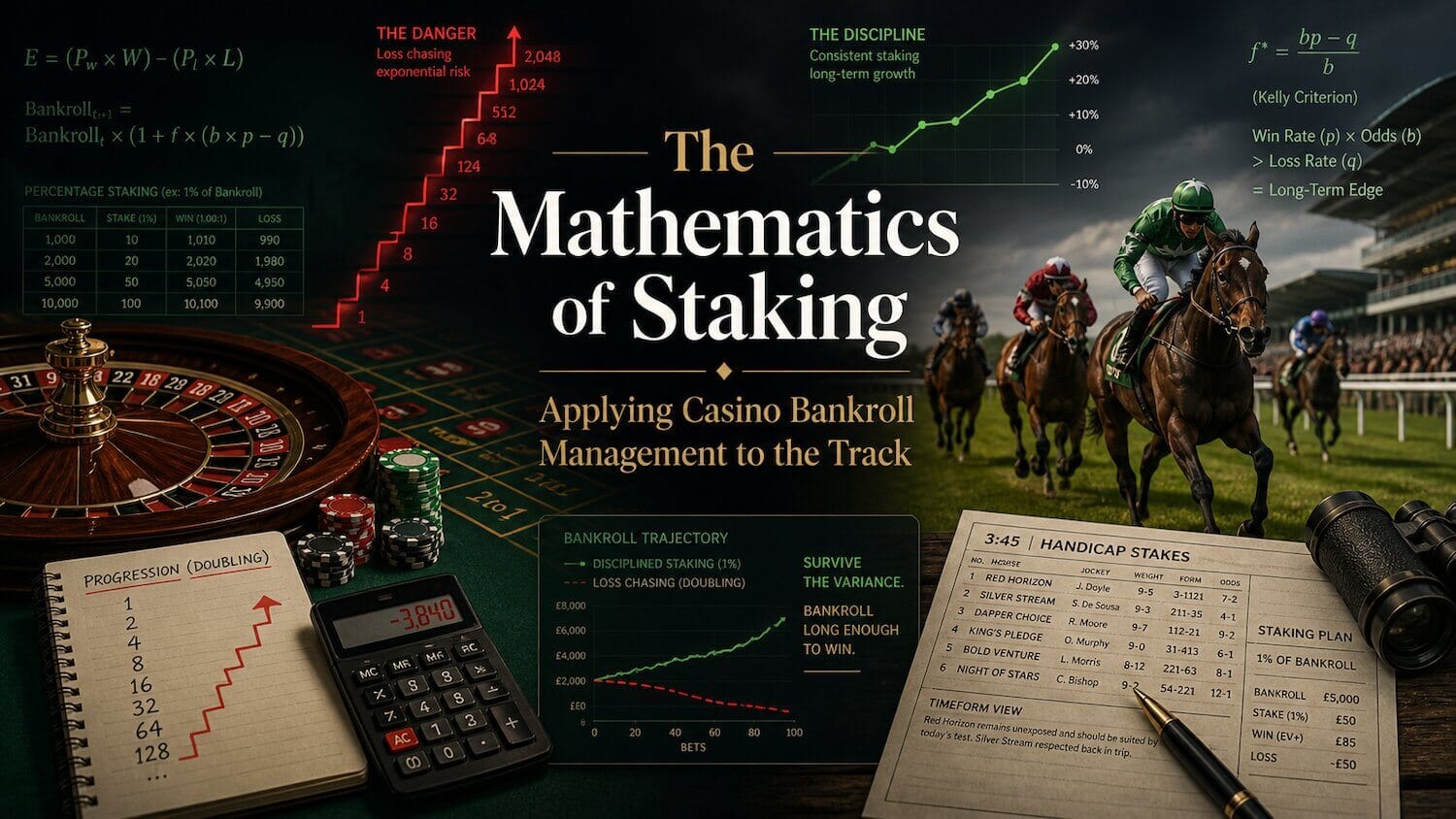

What makes loss-chasing dangerous is that it doesn’t feel reckless — it feels mathematical. A slightly larger stake on a slightly shorter price will, the reasoning goes, recover the day. The casino floor has been studying this exact pattern for three centuries, and the staking systems players invented to combat it expose the underlying logic in its purest form.

According to rouletteuk.co.uk, a site comparing various roulette systems for uk players, the most enduring of these systems — Martingale, Paroli, D’Alembert, Fibonacci — all share one feature: they prescribe stake sizes based purely on the previous result, with no reference to the underlying probability of the next one. Understanding why that fails is the fastest route to seeing what’s wrong with the loss-chase argument inside your own head.

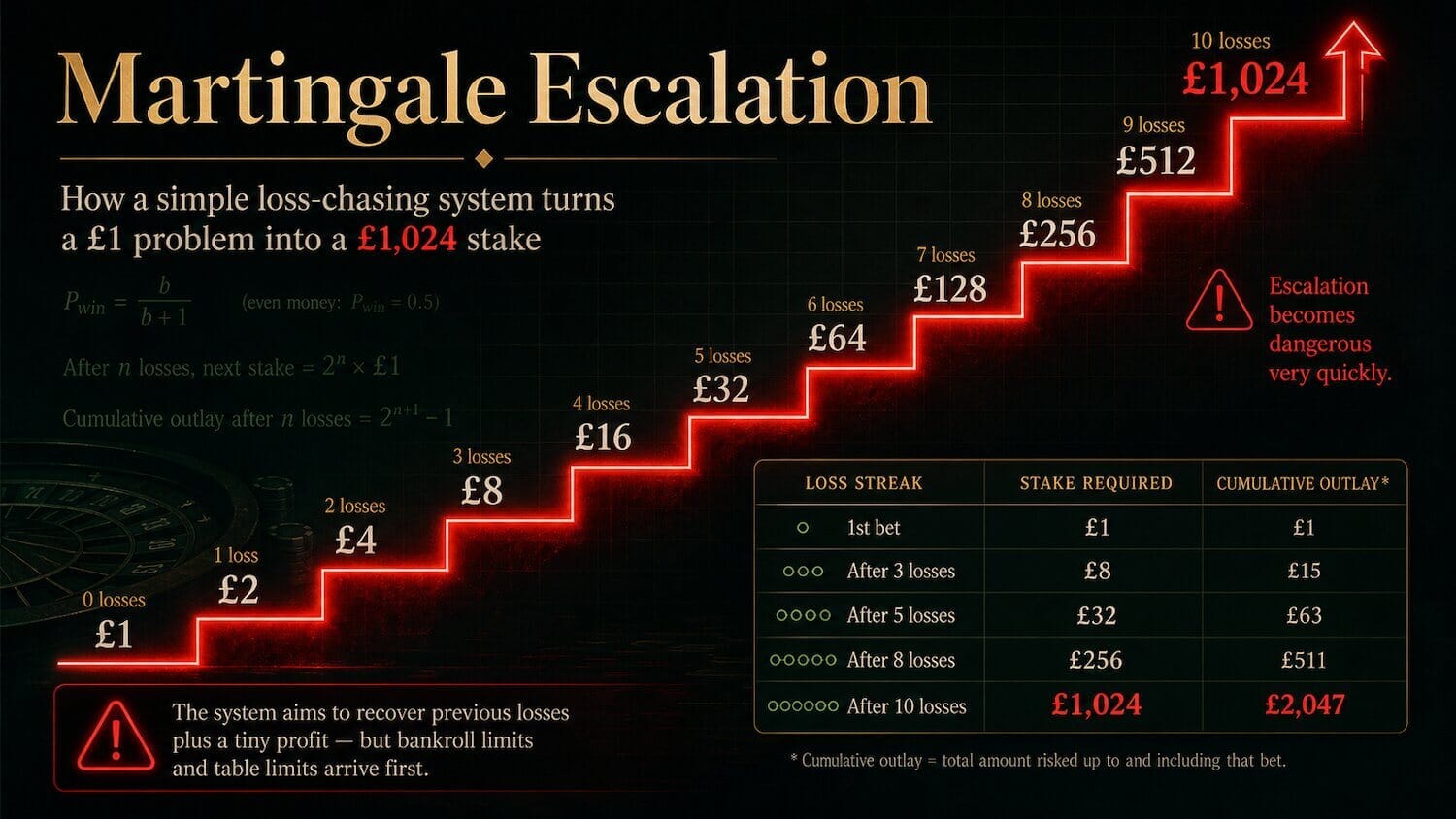

The Martingale: discipline as illusion

The rules are simple: bet one unit on an even-money proposition. After a loss, double your stake. Keep doubling until you win, then reset. Each win recovers all previous losses plus a single unit of profit.

It looks like discipline. It performs like discipline — for a while.

| Loss streak | Stake required | Cumulative outlay |

| 1st bet | £1 | £1 |

| After 3 losses | £8 | £15 |

| After 5 losses | £32 | £63 |

| After 8 losses | £256 | £511 |

| After 10 losses | £1,024 | £2,047 |

A run of ten consecutive losses on a near-evens proposition occurs roughly once every thousand sequences. Small, but not rare enough — anyone who bets often enough will eventually meet it. When they do, they’ve staked over £2,000 to recover £1, and either the bookmaker’s limit or the punter’s bankroll runs out first.

The same trap turns up at the racetrack in disguise. A punter who lost £40 on the first race of a Saturday card backs the second favourite for £80 in race two. When that loses, the third bet is £160 on whatever looks “safe” — usually a short-priced favourite they wouldn’t have touched at the start of the day. Three losing bets in, the day’s outlay is £280 and the original £40 was the only stake that had ever been reasoned through. That’s Martingale by another name, and the only thing missing is the table to play it at.

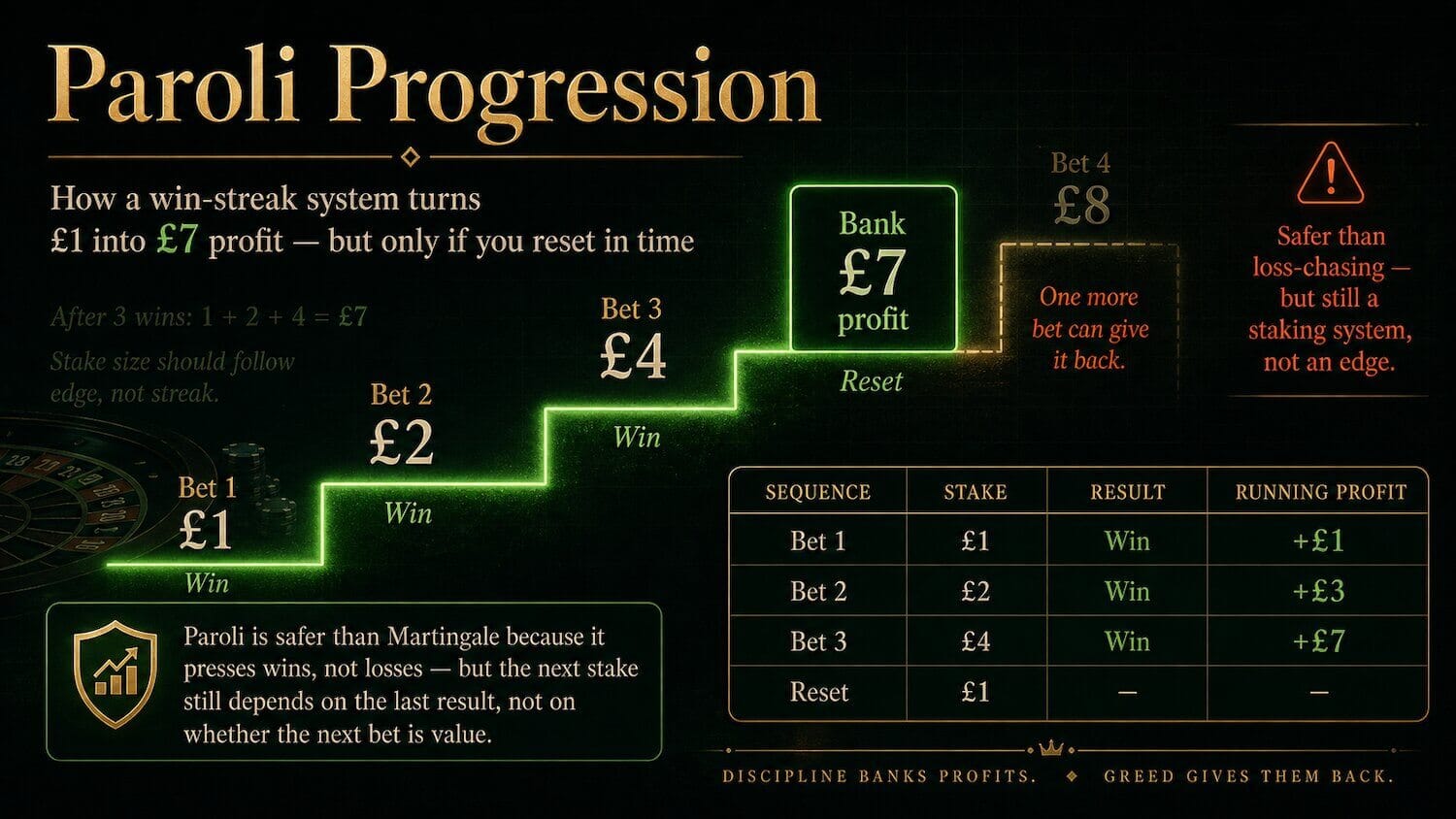

The Paroli: the other side of the same coin

The Paroli reverses direction. Bet one unit. After a win, double the next stake. After three straight wins, bank the profit and reset. After any loss, reset.

| Sequence | Stake | Result | Running profit |

| Bet 1 | £1 | Win | +£1 |

| Bet 2 | £2 | Win | +£3 |

| Bet 3 | £4 | Win | +£7 |

| Reset | £1 | – | – |

Less destructive than Martingale because the bankroll is never asked to absorb a runaway sequence. But the deeper flaw is identical: the rules generate stake sizes that have nothing to do with the punter’s edge on the bet in question. The racing equivalent is the punter who lets winnings ride into bigger and bigger stakes through a hot afternoon, then gives the lot back on the last race — because the rules of the system never asked whether the last bet was actually a value bet, only whether the previous one won.

What this means for racing bankrolls

Staking determines how a bankroll absorbs variance. It does not, and cannot, create an edge where none exists. Every progression system is an attempt to dodge that fact, and every one of them eventually fails for the same reason.

What survives a season is much less dramatic.

| Method | How it works | Trade-off |

| Level stakes | Same fixed unit on every selection | Simple, transparent, exposes edge cleanly. Doesn’t compound. |

| Percentage staking | Fixed share of current bankroll (typically 1–3%) | Adjusts to bankroll size, prevents ruin, naturally slows during losing runs. Requires honest bookkeeping. |

| Kelly criterion | Stake proportional to perceived edge | Mathematically optimal for compounding — but only if your edge estimate is accurate. Most punters overestimate, so half-Kelly or quarter-Kelly is the practical version. |

For the average punter, percentage staking is the most useful of the three. With a £1,000 bankroll and a 2% unit, every selection gets £20. After a £200 losing run, the unit drops automatically to £16. After a £200 winning run, it climbs to £24. The plan adjusts to reality without the punter having to make a decision in the moments when their judgement is at its worst — which is the entire job a staking plan should be doing.

Spotting the chase before the chase

A staking plan only works if the punter follows it. The signs a plan is about to be abandoned are usually visible before the abandoning bet goes on:

- Recalculating mid-meeting what stake “gets the day back”

- Adding selections that weren’t on the morning’s shortlist

- Backing shorter prices than usual to make the recovery cleaner

- Telling yourself this race is the exception

- Backing horses you wouldn’t have looked twice at four hours earlier

- Increasing stake size after a tip you didn’t act on came in for someone else

Each of these is the racing equivalent of doubling after a Martingale loss. The math feels reassuring; the bankroll arithmetic is anything but.

Bottom line

The casino-floor systems aren’t models for racing punters to copy. They’re a mirror. They show, in stripped-down form, what happens when staking is asked to do a job — generating profit from thin air — that staking cannot do. The disciplined racing punter is the one who has internalised the distinction: stake size protects the bankroll, selection generates the edge, and the worst day at the meeting is the day those two get confused.